In recent years, the financial world has been steadily shifting from traditional banking to more agile and specialized digital ecosystems. Fintech startups – not legacy institutions have emerged as the primary drivers of this transformation, offering tailored financial tools built around technology. Spend.net is one such platform, offering virtual USD cards without the standard restrictions of traditional banks.

A Different Model: Spend and Earn

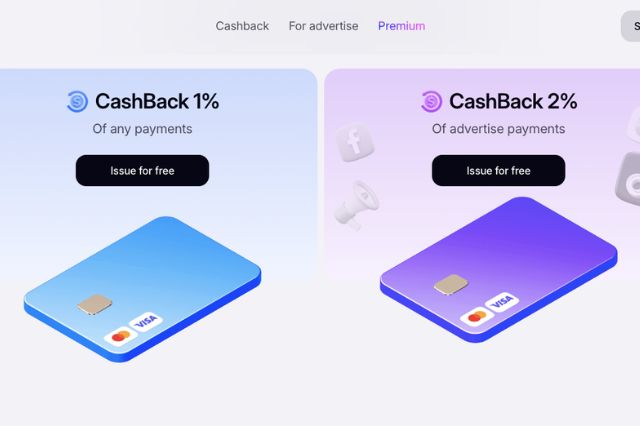

Spend.net sets itself apart with a built-in universal cashback mechanism. Users earn 1% back on every transaction, regardless of category. Unlike limited-time offers or merchant-specific rewards, Spend.net’s cashback applies across all online purchases with no exceptions.

This approach, often referred to as “universal cashback,” is rare in the broader consumer segment due to its high operational demands. But for Spend.net, it’s a core value proposition — enhancing user loyalty through consistent, transparent rewards.

Purpose-Built Cards For Diverse Use Cases

Spend.net cards are designed around two core use cases:

- Media buying — tailored for advertisers running campaigns on Google, TikTok, and Facebook

- Personal expenses — versatile cards for subscriptions, e-commerce, and everyday digital payments

All cards are issued via Visa or Mastercard, ensuring compatibility with most online platforms and services globally in 2025.

Rethinking Fees: Flexibility Over Fixed Rates

One of Spend.net’s most innovative features is its top-up fee structure. Rather than enforcing a fixed percentage, users choose the commission rate that suits their payment scenario, whether it’s a one-time high-volume deposit or recurring micro-top-ups.

There are no hidden fees. The platform charges:

- 0% on all transactions

- 0% on refunds and declined payments

- 0% on withdrawals

- 0% on FX transactions

The only exception is a minimal service fee for top-ups under $50. This transparent fee model is especially relevant for businesses managing tight advertising budgets where cost predictability is essential.

Security and User Experience

Spend.net cards support 3D Secure by default, meaning every transaction requires one-time SMS verification. This adds a strong layer of fraud protection and aligns with global security standards.

Crypto Integration: Top Up With USDT and BTC

Spend.net also caters to crypto users, allowing account top-ups in USDT and BTC. For freelancers, digital nomads, and crypto-native professionals, this makes Spend.net a seamless bridge between crypto holdings and day-to-day spending. According to Chainalysis, up to 28% of virtual card users in 2024 regularly use USDT for everyday payments — a trend that Spend.net clearly supports.

Instant Setup, No Verification Required

Time is a critical asset, and Spend.net minimizes onboarding friction. Users can register via Google (in under 30 seconds) or with an email address. No KYC is required, and cards are issued instantly. Users can generate as many cards as needed, making the platform ideal for ad buyers running multiple campaigns using the “one card per campaign” strategy.

24/7 Support: Real-time Problem Solving

Spend.net provides round-the-clock support via live chat. This is essential for global users operating across time zones or managing advertising campaigns outside regular business hours.

Final Thoughts: A FinTech Tool For The Digital Economy

Spend.net is not just another card issuer. It’s a modern fintech tool designed to integrate directly into how digital-first users operate — whether in business or personal finance. With flexible fees, universal cashback, crypto integration, and real-time support, Spend.net positions itself as a practical, no-nonsense solution for anyone seeking operational efficiency without unnecessary bureaucracy.

In a world where spending efficiency matters and the lines between personal and professional finance continue to blur, platforms like Spend.net aren’t just useful — they’re inevitable.

Related

{kind=link}

{kind=link}